If you're reading this, there's a good chance your bank account hits near-zero a few days before payday — every month, like clockwork. You're not alone. According to recent surveys, over 60% of Americans and nearly half of Canadians live paycheck to paycheck, including many people earning well above median income.

The problem usually isn't income. It's the gap between what comes in and where it quietly disappears before you notice. This guide covers exactly how to close that gap — with practical steps, not generic advice.

Why this keeps happening (it's not what you think)

Most paycheck-to-paycheck cycles aren't caused by overspending on luxuries. They're caused by three structural problems:

Invisible spending

Subscriptions, small recurring charges, and "set and forget" expenses you stopped noticing years ago. The average American has 4–6 active subscriptions they've forgotten about.

Lumpy expenses

Car registration, insurance renewals, medical bills, holiday spending — these aren't monthly but they wreck monthly budgets. Without a plan for them, they hit like emergencies every time.

No buffer

Without even $500–$1,000 sitting in a separate account, every unexpected expense (a parking ticket, a vet bill) resets your progress and forces you to borrow from next month's money.

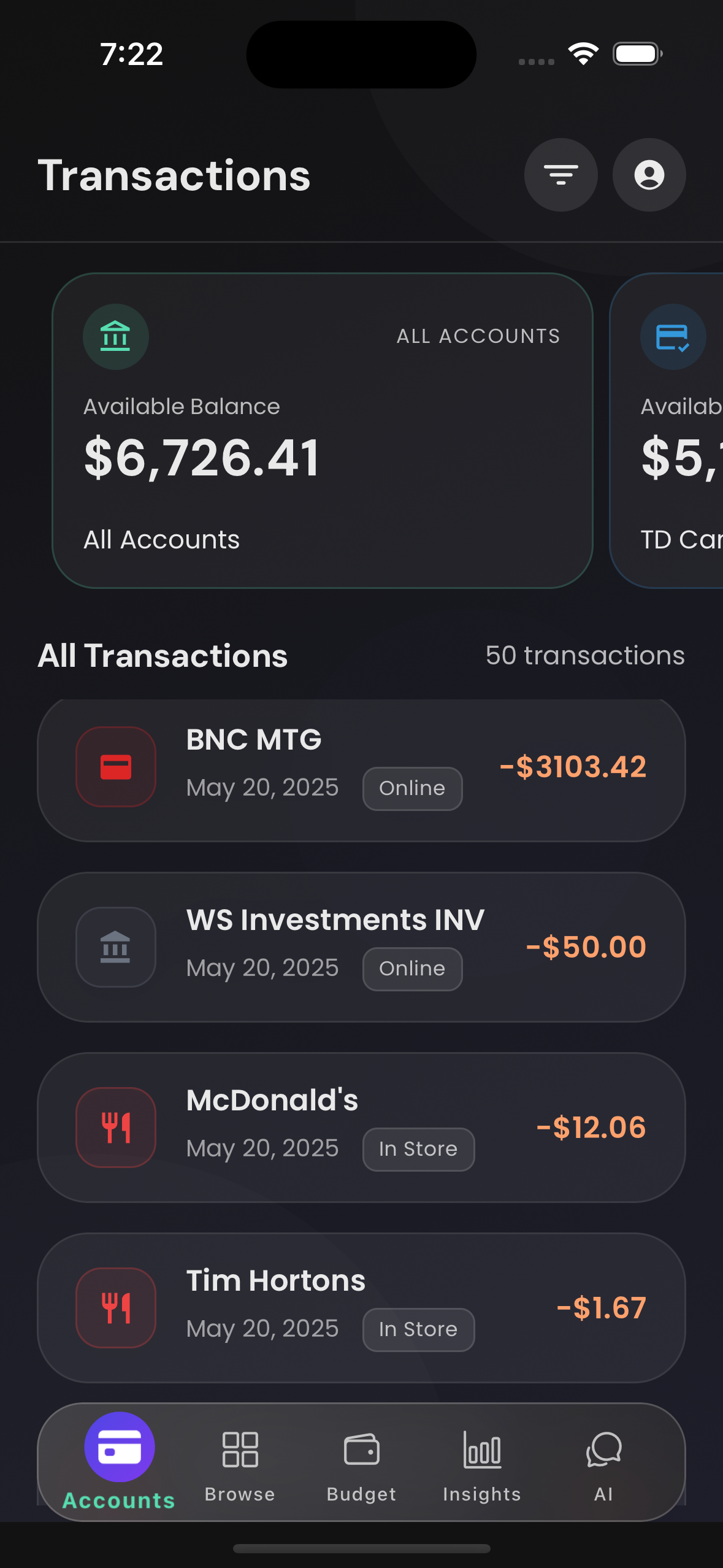

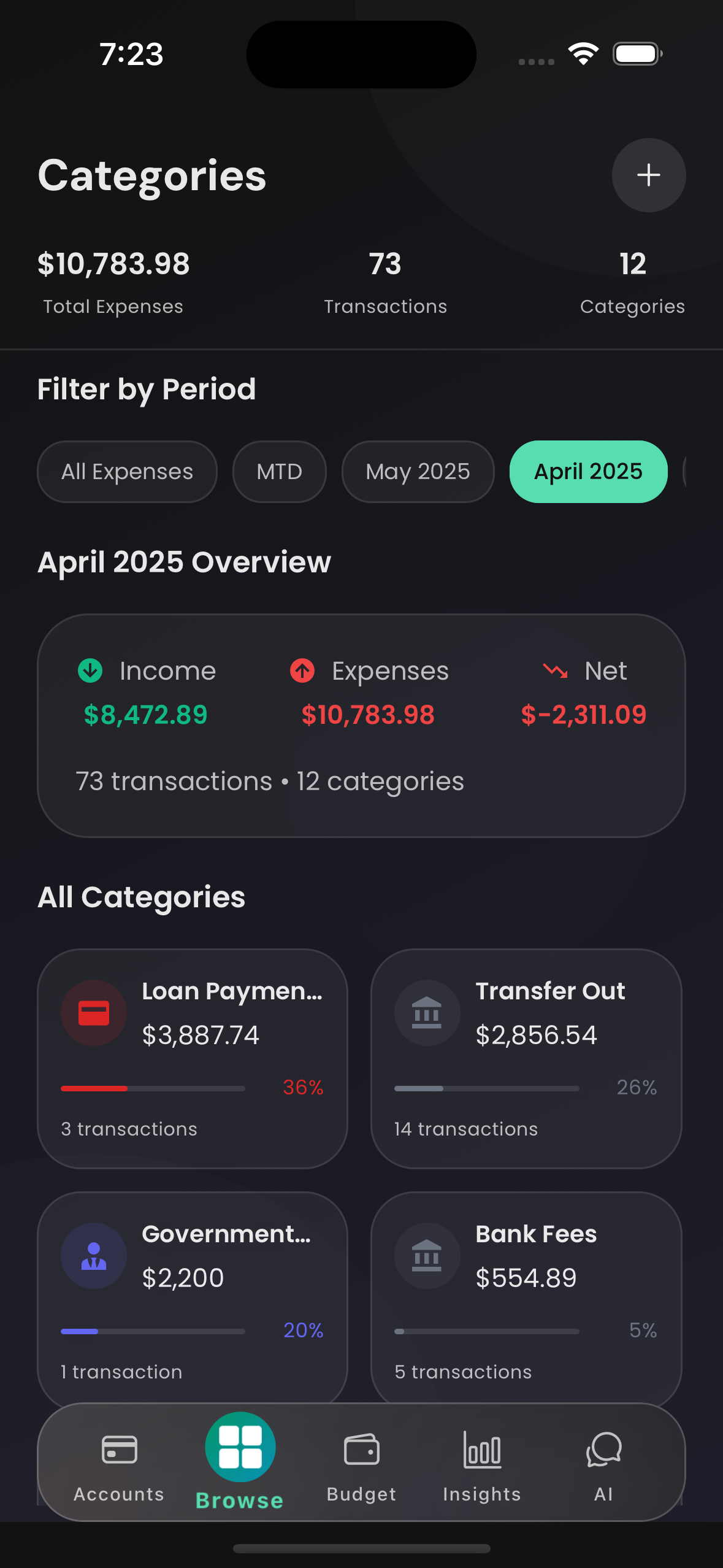

Step 1: See exactly where your money goes (this week)

Before changing anything, you need a clear picture. Not an estimate — the actual numbers. Connect your bank accounts to a tracking app and look at every transaction from the last 60 days.

Most people discover two things: (1) they're spending more in 2–3 categories than they thought, and (2) there are recurring charges they completely forgot about. Both are fixable once you can see them.

Common spending surprises people find

All transactions in one view

Spending by category

Step 2: Build a one-month buffer (your actual goal)

The real exit from the paycheck-to-paycheck cycle isn't cutting lattes — it's building a buffer between your income and your expenses. When you have $1,000–$2,000 sitting in a separate account that you don't touch, unexpected expenses stop being crises.

Start small. Your first target is $500. That covers most car problems, most medical co-pays, and most appliance failures. It's not an emergency fund — it's a cycle-breaker.

$500

Cycle-breakerCovers most unexpected bills without borrowing from next month

$1,000

Stability bufferHandles larger emergencies — car repair, dental, flights

1 month of expenses

True bufferYou're no longer living paycheck to paycheck by definition

3–6 months

Emergency fundJob loss, health crisis, major life disruption — you're covered

Step 3: The "pay yourself first" system

Most people try to save whatever's left at the end of the month. There's never anything left. The fix is to move savings to a separate account on payday, before you spend anything — even if it's just $50 or $100.

Set up an automatic transfer the day after your paycheck hits. You'll adjust your spending to whatever's left, because humans are remarkably good at living within their means when the money isn't visible.

"Don't save what's left after spending. Spend what's left after saving." — Warren Buffett

Step 4: Handle the irregular expenses

List every expense that hits less than monthly: car insurance, renters/home insurance, registration fees, subscriptions billed annually, holiday gifts, back-to-school, summer vacation. Add them all up and divide by 12.

That number — let's call it your "sinking fund" amount — should be transferred to a separate savings account every month. When those irregular bills arrive, they're already paid for. This single habit eliminates most "emergency" spending.

Example: Annual irregular expenses

Set aside $292/month and none of these feel like emergencies

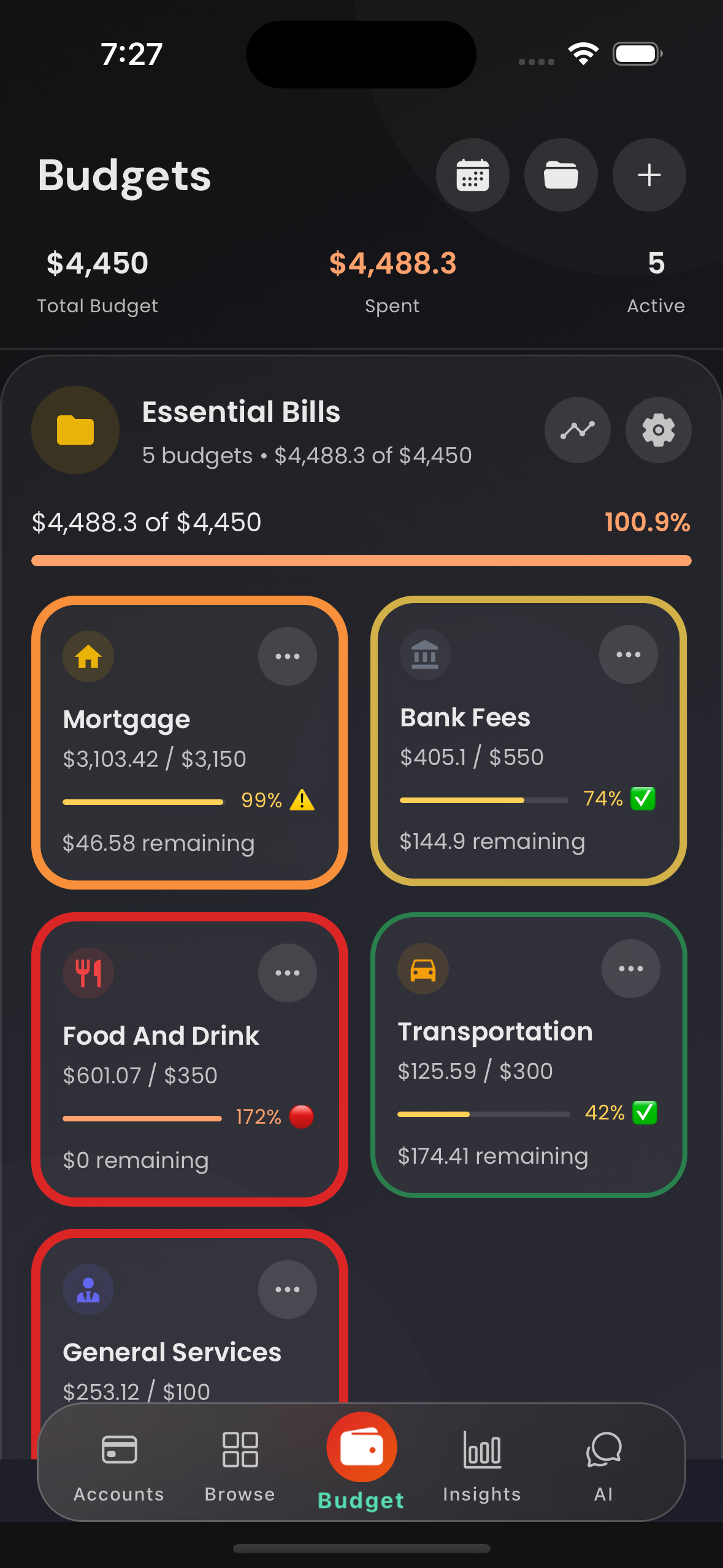

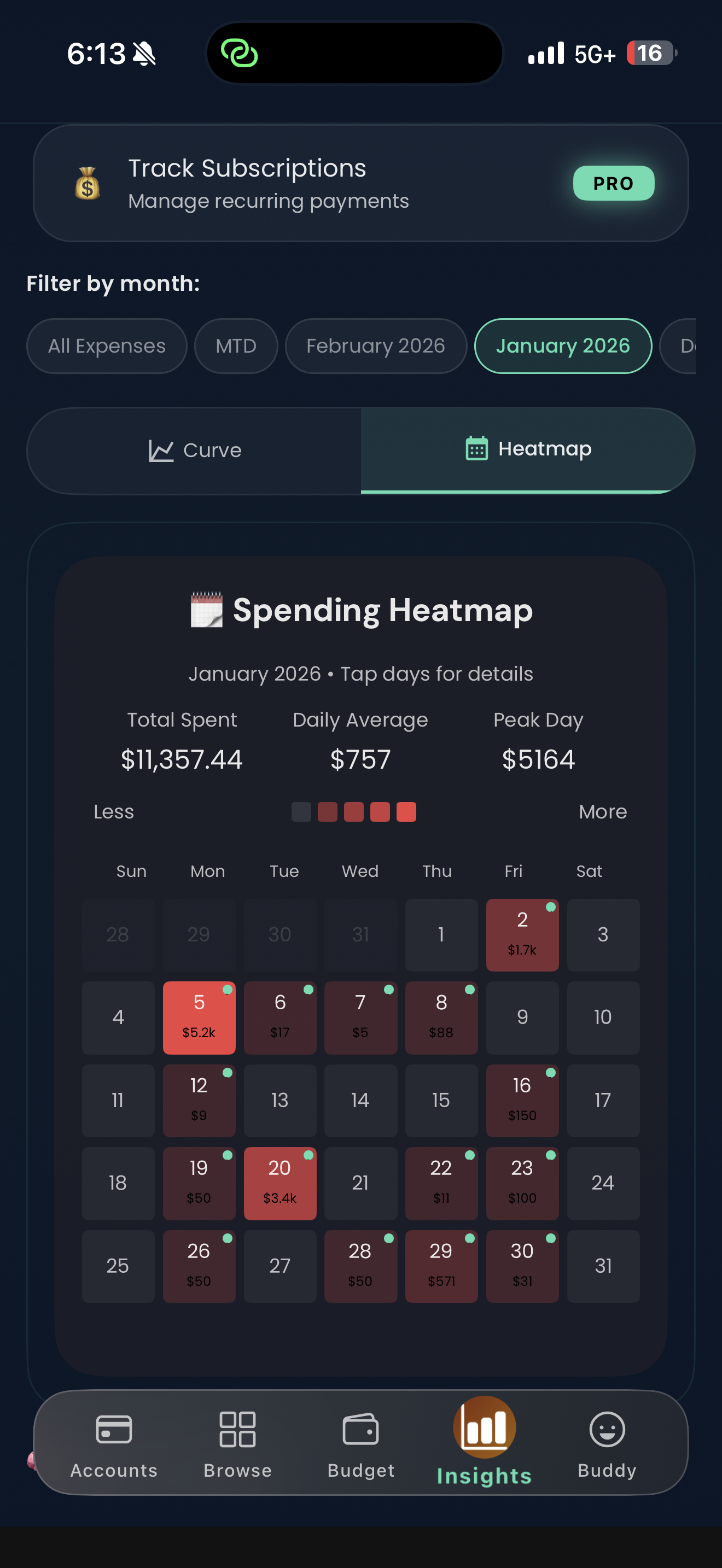

Step 5: Set spending limits — and actually track them

A budget only works if you know where you stand mid-month, not just at the end. Set a limit for the 2–3 categories where you overspend most (usually dining, shopping, and entertainment). Check it once a week — not obsessively, just once.

Budget limits with progress

Spending heatmap by day

How long does this actually take?

Most people who follow these steps consistently see a meaningful change within 60–90 days. Not because their income changed — because they stopped leaking money in ways they couldn't see.

The short version

- See where your money actually goes — not what you think, the real numbers

- Build a $500 buffer before anything else

- Automate savings on payday, before you spend

- Account for irregular expenses monthly so they stop hitting like emergencies

- Set limits in your 2–3 highest-spend categories and check them weekly

None of this requires cutting everything you enjoy. It requires knowing your numbers clearly enough to make intentional decisions — and that starts with being able to see them.