Most budgeting guides start with a spreadsheet and end with you overwhelmed three days later. This one is different. I'll give you the actual steps — in the order they should happen — without the filler.

The pattern I've seen: people know they should budget, they're not sure where to start, they try something, it doesn't stick. The problem usually isn't motivation. It's the wrong system for how they actually live.

Step 1: Find your real take-home income

Before any budgeting can happen, you need one number: what actually lands in your account each month after tax and deductions. Not gross salary. Not what you think you make. The real deposit.

For salaried Canadians, check your last two pay stubs. For variable income (freelance, hourly, commission), use your lowest month in the last six as your baseline — budget from that, and anything above it is a bonus.

Rough Canadian take-home estimates

After federal + provincial tax, CPP, EI. Varies by province.

These are estimates. Always use your actual pay stub.

Step 2: Track before you cut

This step is counterintuitive. Most people want to immediately set restrictions. Don't — not yet. Spend one month just tracking without changing anything. The goal is to see your actual habits, not your idealized ones.

The easiest way is connecting your bank accounts to an app that auto-categorizes every transaction. You'll find subscriptions you forgot about, spending patterns you didn't realize existed, and a clear picture of where the money actually goes.

Saveo auto-categorizes every transaction from your Canadian bank accounts

Step 3: The 50/30/20 rule (treat it as a target, not a law)

The 50/30/20 rule is the most practical starting framework for most people:

Needs

Rent or mortgage, groceries, utilities, transit, insurance, minimum debt payments

Wants

Dining out, entertainment, subscriptions, shopping, travel

Savings & debt

RRSP, TFSA, emergency fund, extra debt payments

The honest reality for most Canadians in major cities: housing alone often takes 35–45% of take-home, which pushes needs well past 50%. That's fine. If your needs are at 60%, aim for 20% wants and 20% savings rather than stressing about the ideal split.

Step 4: Set category budgets with real numbers

Once you've tracked a month of actual spending, set monthly limits by category. The key ones to start with:

- Groceries — most Canadians underestimate this. Average household spends $1,100–1,400/month (Statistics Canada 2024)

- Dining out — track separately from groceries. This is where most overspending happens

- Subscriptions — do a full audit. Netflix, Spotify, iCloud, gym, apps, news — they add up quietly

- Transportation — gas, insurance, transit pass, parking, car payments

- Entertainment / personal — give yourself a real number here. $0 fun budgets don't last

Set budgets with live progress bars

Category spending breakdown

Step 5: Set up alerts — this is what makes budgets actually stick

Budgets fail when you don't know you're over them until after the month ends. The fix is simple: set spending alerts at 75% and 100% of each category. A notification at 75% gives you time to adjust. At 100%, you at least know what happened.

The two-alert system

75% alert: You still have room to adjust. This is the one that saves you.

100% alert: You've hit the limit. No judgment — but you need to know.

Canadian-specific things worth knowing

TFSA vs RRSP — where should savings go?

Short version: if you're earning under ~$55,000/year, prioritize TFSA contributions. If you're above that, RRSP contributions give a meaningful tax deduction. When in doubt, TFSA first is almost always the safe call — the withdrawal flexibility alone is worth it.

Province matters more than you think

Someone earning $80,000 in Alberta takes home meaningfully more than the same salary in Quebec or Ontario. Always build your budget from your actual provincial take-home, not national averages.

Don't overlook GST/HST credits and Canada Child Benefit

These aren't just for low-income households — the income thresholds are higher than most people expect. If you have kids or earn in a lower bracket, these can meaningfully change your effective monthly budget.

Cash flow over time

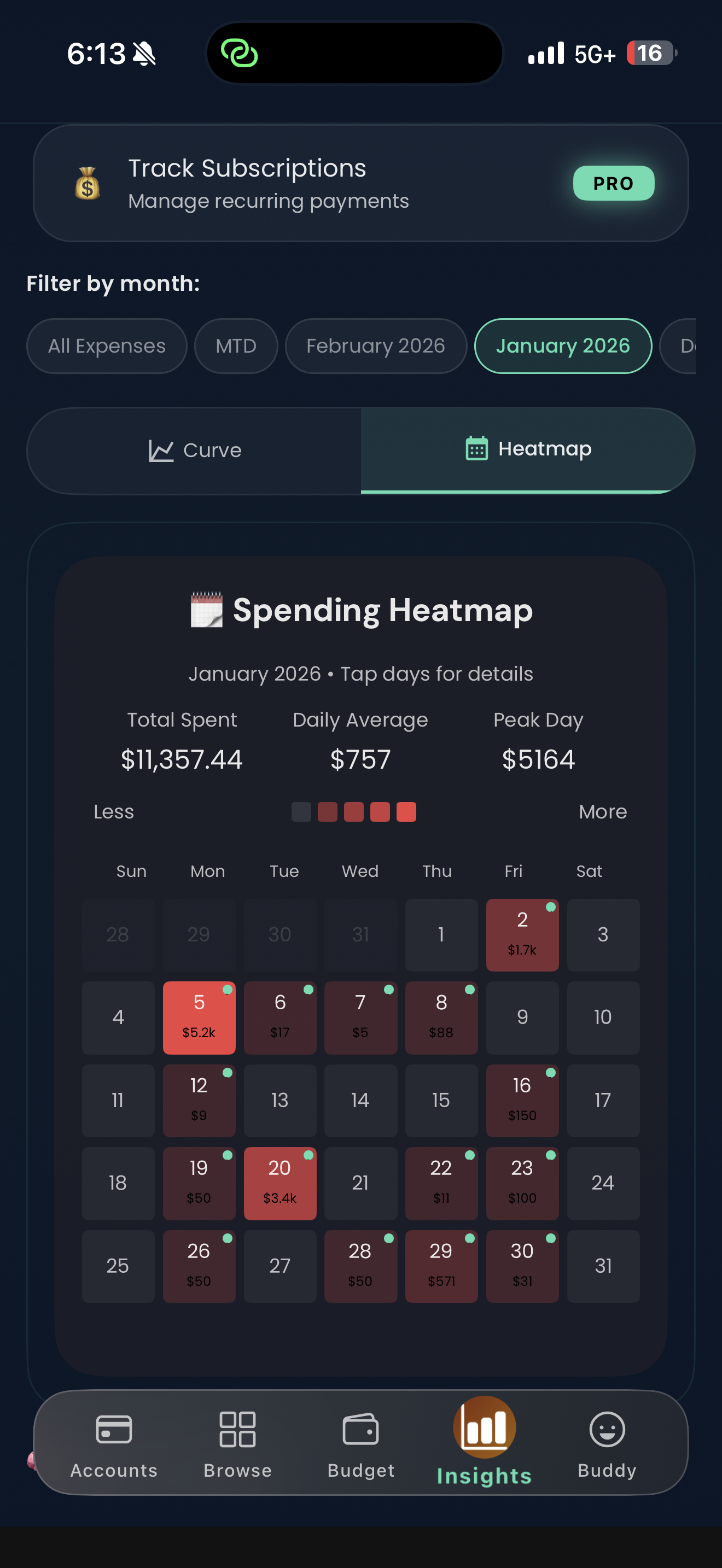

Daily spending heatmap

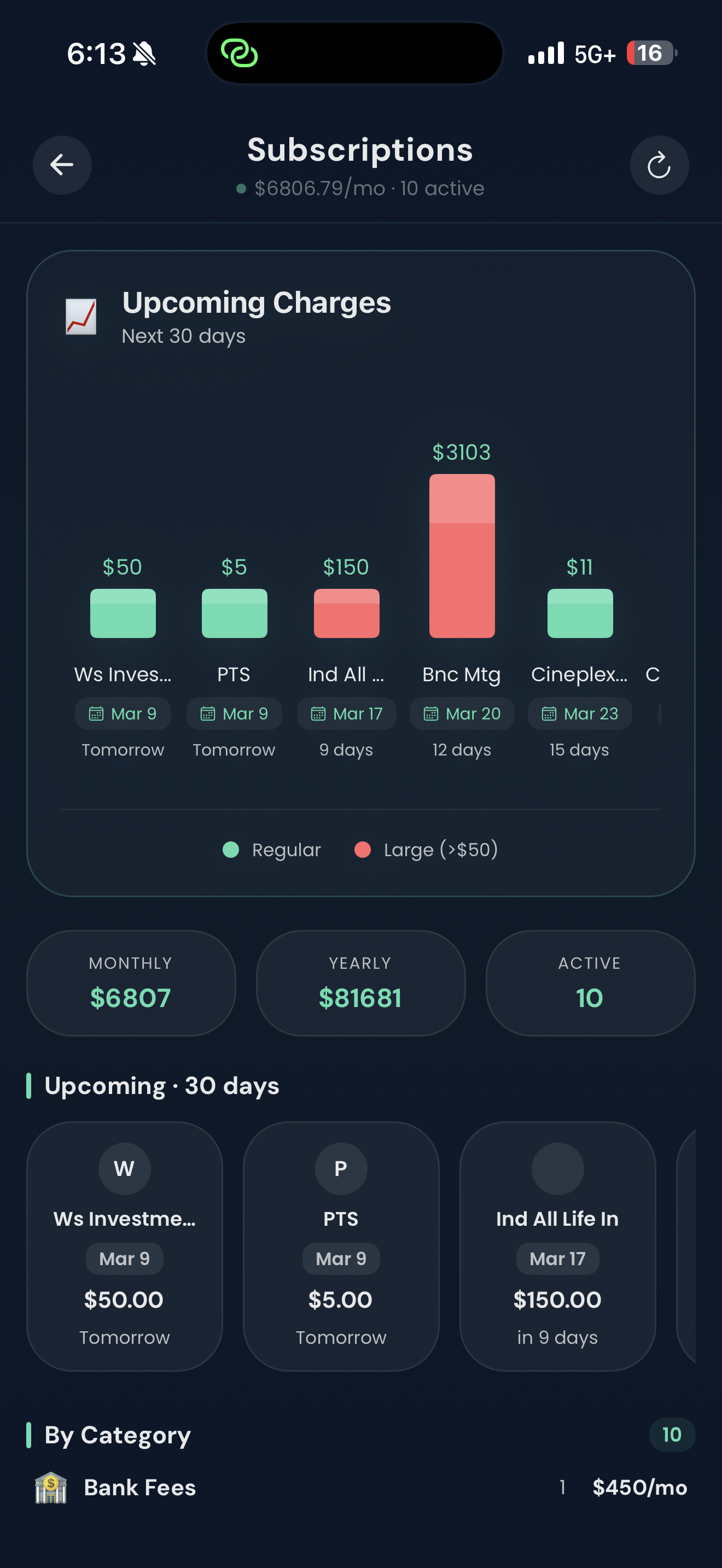

Subscription tracking

The most common budgeting mistakes Canadians make

- Budgeting from gross salary — always use your actual take-home

- Setting a $0 fun budget — it won't last. Give yourself a real, guilt-free spending allowance

- Forgetting annual expenses — car insurance renewal, yearly subscriptions, holiday spending. Divide by 12 and budget monthly

- Only reviewing once a month — check in weekly, even briefly. Five minutes keeps you on track

- Investing before building an emergency fund — aim for 3 months of expenses in a HISA first

Start today, not next month

Every month you delay is a month of data you don't have. You don't need a perfect system — you need one that starts. A rough budget you actually use beats a perfect one you build next month.

Connect your bank accounts, look at where your money went last month, and set three category budgets. That's all it takes. Everything else follows from having real numbers in front of you.